Over the past few years I’ve been increasing the amount I give to charity*.

As giving has taken up a larger proportion of my income, I’ve done some digging into the rules around donating to charity – specifically those on tax – to see how I might be able to give more with the amount I have.

While the obvious things are easy, finding and getting my head around the relevant tax rules took longer than I expected. In the hope of saving someone else (and future me!) some time, here’s my current understanding.

Note: I’m not an accountant, and I’m definitely not qualified to give tax advice. Almost everything here comes from the tax relief section on the gov.uk website. Before making any decisions, check that what I’ve written is correct and applies to your situation!

Summary – key things to know about UK income tax and giving to charity:

- UK charitable donations are fully tax-deductible.**

- Some of the tax relief can go to your chosen charity automatically (i.e. ‘Gift Aid’).

- You might be eligible for extra tax relief, which you can claim back by asking HMRC to reduce your tax bill.

- Extra tax relief can be significant! Depending on your tax rate, tax relief can give you a 1.25x-2.5x donation multiplier.

- There’s some flexibility around which tax year you account for donations in. If you’re earning less this year than last year you might be able to significantly reduce your tax bill this way!

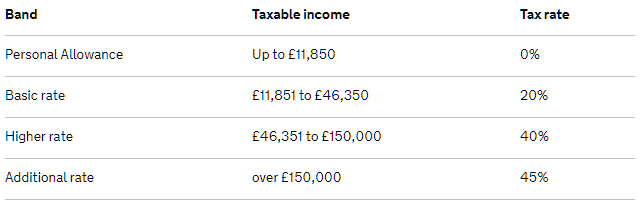

How UK Income Tax Works

Before we go into donations and claiming tax back, a brief summary of UK income tax.

UK income tax is progressive, i.e. increases with income.

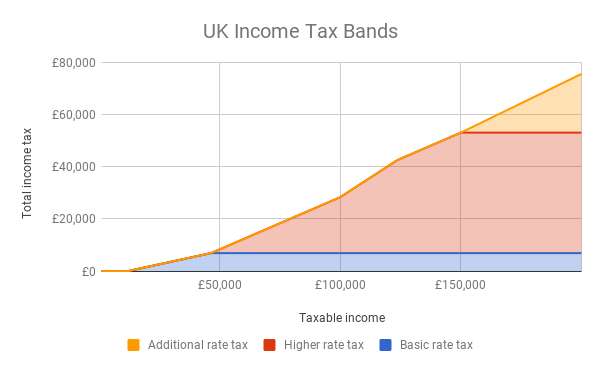

The chart below shows what total income tax looks like for various income levels, and how that breaks down into the various bands. I’ve included data up to £200k since beyond that it just goes up linearly, and if you’re in that band you should probably consider investing in proper tax advice!

A few things you’ll notice about the chart:

- If you earn less than £11.85k per year, you pay no tax.

- As you go further to the right from there, you always pay more tax overall.

- The top line generally gets steeper as you go right, but this isn’t true everywhere.

- The steepest part of the chart is between £100k and £123.7k, where you gradually lose your personal allowance.

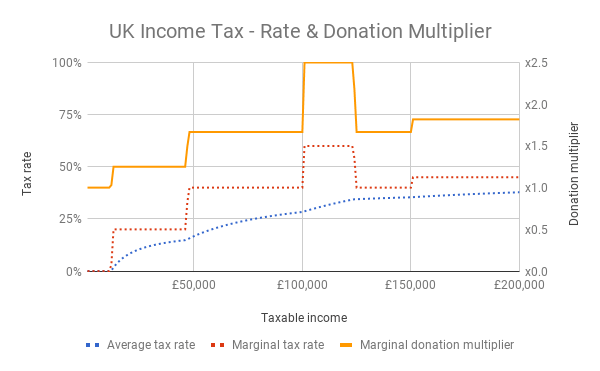

The steepness of that top line represents your marginal tax rate – i.e. how much tax you’ll pay on every extra £1 you earn at that level. This is a useful thing to look at, because it affects the ‘donation multiplier’ you’ll get at that level – i.e. how much your chosen charity will get for every £1 in net income you give up.

Here’s another chart which shows that relationship more clearly:

While your average tax rate might be interesting to you, the marginal tax rate is generally more useful (unless you’re planning on donating 100% of your income!).

What does this second chart show? Pay attention to the yellow line, showing the donation multiplier for £1 at each level:

- When you earn below £11.85k, your donation multiplier is x1. This makes sense, since there’s no tax to deduct. For every £1 you give to charity, you lose £1.

- When you earn £11.85k-£46.35k, your donation multiplier is x1.25. If you’re in this bracket, you’re in luck – your tax deduction is fully taken care of by Gift Aid, so all you have to do is remember to tick that box when you donate and the charity gets an extra 25% directly from the government.

- In the bracket £46.35k-100k and again from £123.7k-£150k, your donation multiplier is x1.67. At this point the 25% in Gift Aid doesn’t fully cover your tax deduction, so you get to claim back some extra tax from HMRC (see below for more on how to do this).

- At £100k-£123.7k, not only are you in the top 0.1% of global earners, but you’ve hit the donation multiplier sweet spot of x2.5. You can more than double your*** money with every donation! You can give £2.5 to charity and lose only £1. This is because you’d be paying 40% in tax while your personal allowance would be reduced by 50p for every £1 increase in your salary, resulting in an effective 60% marginal tax rate. Again, you’ll get to claim back a lot of tax on any donations.

- Beyond £150k – congrats! You’re comfortably in the top 0.1% of the global population, earning almost 150x the global average salary. Not only that, your donation multiplier is x1.8, so you only give up 55p for every £1 you give to charity. And giving to charity can raise your tax-free pension allowance.

How to claim tax back

So how does this claiming tax back thing work?

As I’ve covered above, if you’re a basic rate taxpayer (i.e. your total taxable income is up to £46.35k) then you don’t need to worry about claiming tax back – Gift Aid takes care of it.

Beyond that there are three options I’m aware of: Payroll Giving, doing a tax return, or asking HMRC to change your tax code.

Payroll Giving is great, but your employer needs to be set up for it. If they are, then all you need to do is tell your employer your intended monthly donation. They’ll take it straight out of your gross salary and give it to your charity of choice, without any tax being deducted.

If you fill in a Self Assessment tax return, there’s a section on charitable donations. Doing one isn’t exactly fun, but it’s not as difficult as it sounds (and I’ve heard it’s much easier than the US system!). All your employer’s data will be imported already, so you only need to fill in additional details on your donations and any other relevant sections. If you’re doing regular donations then the next option is probably better for you, but if you want to be able to do things like optimising the tax year of your donations then you’ll need to fill in a Self Assessment tax return. And if you earn over £100k you’ll have to do one anyway.

Until fairly recently, I thought those were the only two options. It turns out there’s a third one! If you give regularly and don’t fancy filling in a tax return, you can just ask HMRC to change your tax code. All you need to do is tell them how much you’re donating every month, and they’ll change your tax code to increase your personal allowance – thereby reducing the amount of tax you’ll pay. I think you can probably do this over the phone, but I found their online chat function easy enough. (obviously always make sure you keep a record of all your donations)

When to claim tax back

This might sound niche at first, but it can be very useful and is not so well known.

When you fill in a Self Assessment tax return, you do that for the previous tax year (April-April). And you have until January 31 in the following year to do this.

Now it turns out that you’re allowed to account for donations made in the current year as if they happened last year. Specifically: “you can also claim tax relief on donations you make in the current tax year (up to the date you send your return) if you either: want tax relief sooner, or won’t pay higher rate tax in current year, but you did in the previous year”.

What does this mean? Well, consider an extreme case where last tax year you earned £123k and this year you think you’ll earn £10k. Without this rule you’d get no tax relief on donations made now, but with it you can still get the 2.5x multiplier on your donation by submitting it in your tax return for last year!

Another scenario where this is useful is if it’s coming up to the end of the tax year and you haven’t decided where to donate to yet. As long as you make the donation before you submit your tax return, you’ll be able to count it as taking place this year for tax reasons.

Other things to consider

That’s probably enough on tax for one post. Here are a few other things to consider:

- Which charities will maximise the impact of your donations?

- Should you give now or give later?

- How much should you give right now? Hopefully this post helps you think about the tax aspects of that. You can find the spreadsheet behind each of the charts here (and 2017/2018 version here), including a calculator sheet for any given income/donation amount. Many people have signed the Giving What We Can pledge to donate 10% or more of their income for the rest of their lives.

- Could you donate appreciated assets (like property, shares, or bitcoin) instead of income? In this case you can get Gift Aid on both income tax and capital gains tax.

- Some employers will match your donations, doubling your donations again with no extra effort involved.

- If you don’t live in the UK, you’ll obviously have to follow different rules. Ben Kuhn has a great post on giving in the US.

- If you’re earning a lot but aren’t sure where to give yet, consider setting up a donor advised fund.

- Is earning to give (i.e. maximising your income and resulting donations) the most promising career path for you? Are there other things you should be considering if you want to maximise your impact on the world?

*See this post or Effective Altruism

** In this post I’ve focused on income tax. I haven’t taken into account National Insurance payments in any of the calculations, as these aren’t deductible. I also haven’t modelled the impact on other things like student loan repayments or pension allowance increases. As for income tax, there are some limits to the amount you can claim back, but they’re quite high – “Your donations will qualify as long as they’re not more than 4 times what you have paid in tax in that tax year”.

*** Obviously the recipient charity’s money rather than yours. Still, pretty cool!